19 May 2026

How Subscription Platforms Quietly Transform Fraud Detection in Recurring Credit Transactions

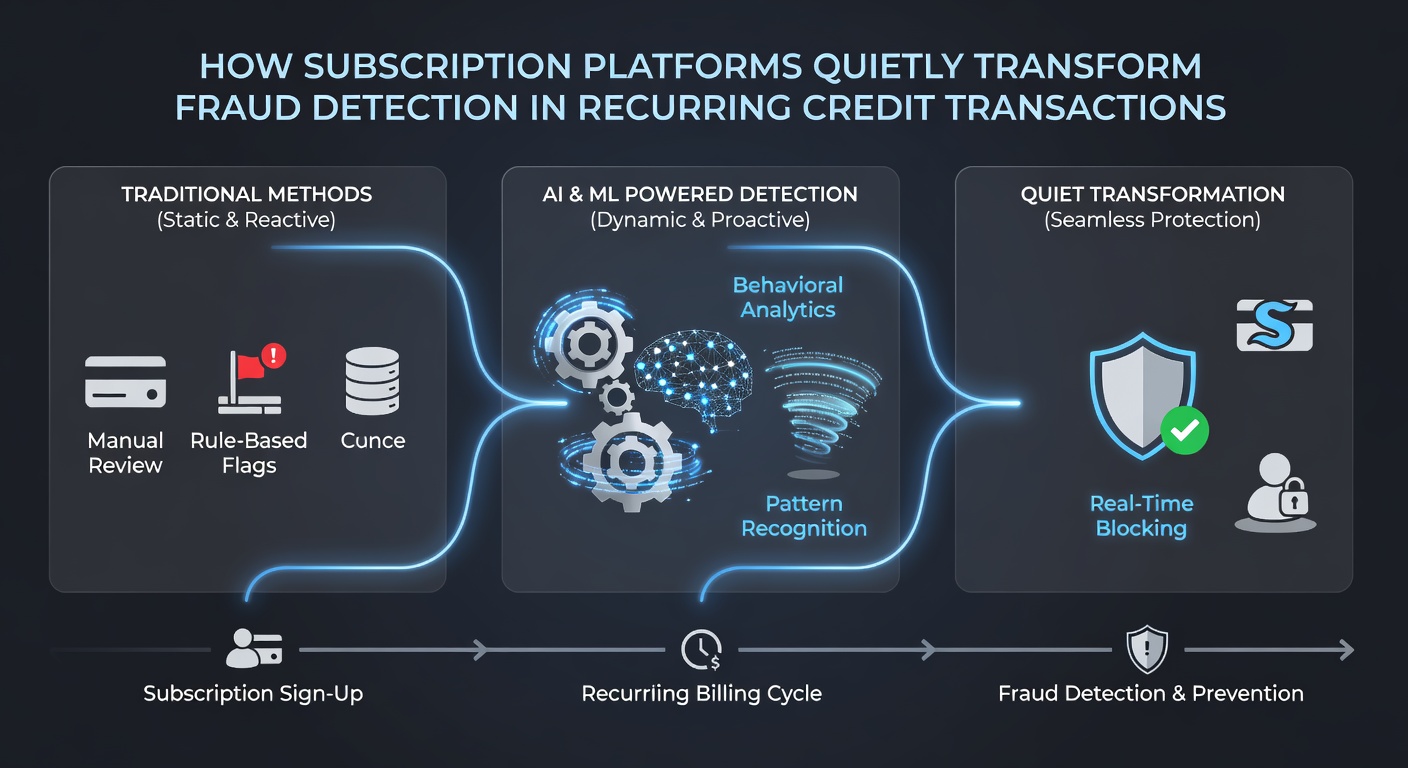

Subscription platforms process continuous streams of recurring credit transactions, which creates unique opportunities for fraud detection systems to evolve beyond one-time payment checks. These platforms collect ongoing data on user behavior, payment patterns, and account interactions, allowing algorithms to identify anomalies that static transaction processors often miss. Researchers have documented how this steady flow of information supports more precise modeling of legitimate activity over months or years.

Continuous Data Collection Shapes Detection Accuracy

Traditional fraud systems rely on isolated transaction details such as amount, location, and device, yet subscription platforms add layers of historical context from repeated billing cycles. Observers note that patterns emerge when a subscriber changes payment methods frequently or accesses an account from multiple regions within short periods, which can signal account takeover attempts. Data from the Consumer Financial Protection Bureau indicates that recurring billing environments generate richer behavioral profiles than single-purchase channels, and these profiles improve machine learning models used for risk scoring.

As of May 2026, several major platforms have expanded their use of longitudinal analysis to track subtle shifts in spending velocity across subscription tiers. This approach helps distinguish between normal upgrades to premium plans and fraudulent attempts to test stolen card limits through small recurring charges. Experts point out that such monitoring occurs in the background without interrupting the user experience for legitimate subscribers.

Behavioral Baselines Reduce False Positives

Subscription services build individualized baselines by analyzing login frequency, content consumption, and renewal timing for each account. When deviations occur, such as sudden spikes in device switches or irregular pause-and-resume patterns, the systems flag potential fraud while allowing routine variations to pass unchallenged. Studies from the University of Toronto's Payment Systems Research Group reveal that these tailored baselines cut unnecessary transaction declines by significant margins compared with generic velocity rules applied across all credit activity.

Platforms integrate these insights with external signals including email reputation scores and linked device histories, creating composite risk assessments that adapt as accounts mature. The result appears in fewer customer service contacts related to blocked legitimate renewals, although the exact mechanisms remain proprietary in most cases.

Integration with Regulatory Frameworks

Regulatory developments in multiple regions have encouraged platforms to refine fraud detection for recurring credit transactions. Australian Securities and Investments Commission guidelines updated in early 2026 emphasize ongoing monitoring of subscription billing to protect consumers from unauthorized charges. Platforms respond by embedding compliance checks into their detection workflows, which simultaneously strengthens fraud prevention and meets disclosure requirements.

European Central Bank reports from the same period highlight similar expectations for continuous oversight of payment service providers handling subscriptions. These overlapping requirements have prompted platforms to share anonymized pattern data through industry consortia, improving collective detection capabilities without exposing individual merchant details.

Real-World Applications in Account Security

One documented case involves a streaming service that noticed clusters of accounts sharing credentials across geographic boundaries, triggering stepped-up authentication before renewal attempts. The platform adjusted its detection thresholds based on aggregate usage data rather than isolated red flags, which reduced successful fraud while maintaining subscriber retention rates. Similar tactics appear in software-as-a-service environments where trial-to-paid conversions create high-value targets for credential stuffing.

Observers note that subscription platforms often detect fraud earlier in the transaction lifecycle because they maintain persistent connections to payment processors. When a card issuer issues a new fraud alert, the platform can propagate that information across all linked recurring schedules in near real time, preventing subsequent charges on compromised credentials.

Conclusion

Subscription platforms continue to influence fraud detection practices by leveraging the repetitive nature of credit transactions to refine behavioral models and response protocols. Research from multiple regulatory and academic sources shows measurable improvements in detection precision as these systems mature through 2026. The quiet integration of continuous monitoring, adaptive baselines, and cross-platform data sharing demonstrates how recurring billing environments serve as testing grounds for broader payment security advancements.