21 May 2026

Inside the Algorithms: How Modern Fraud Prevention Tools Safeguard Recurring Online Transactions for Merchants

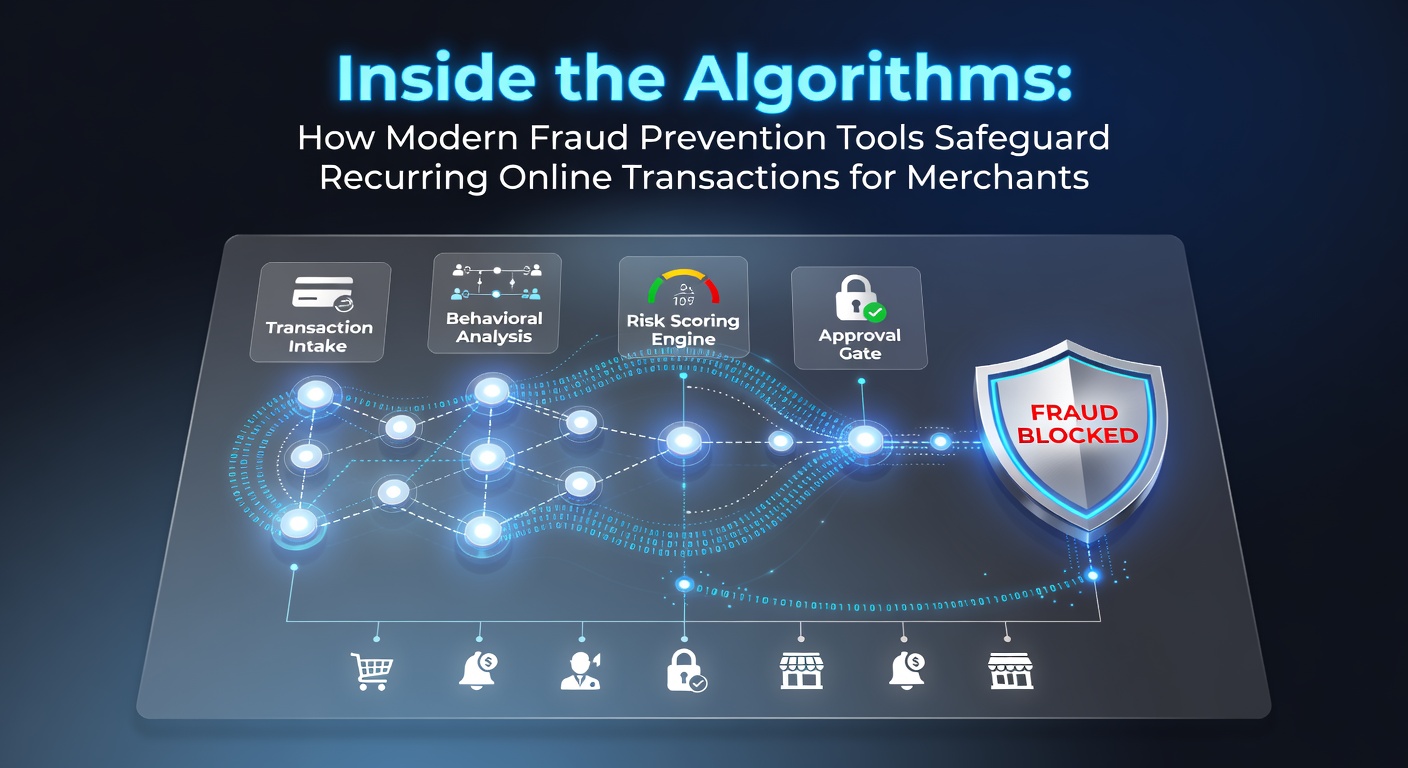

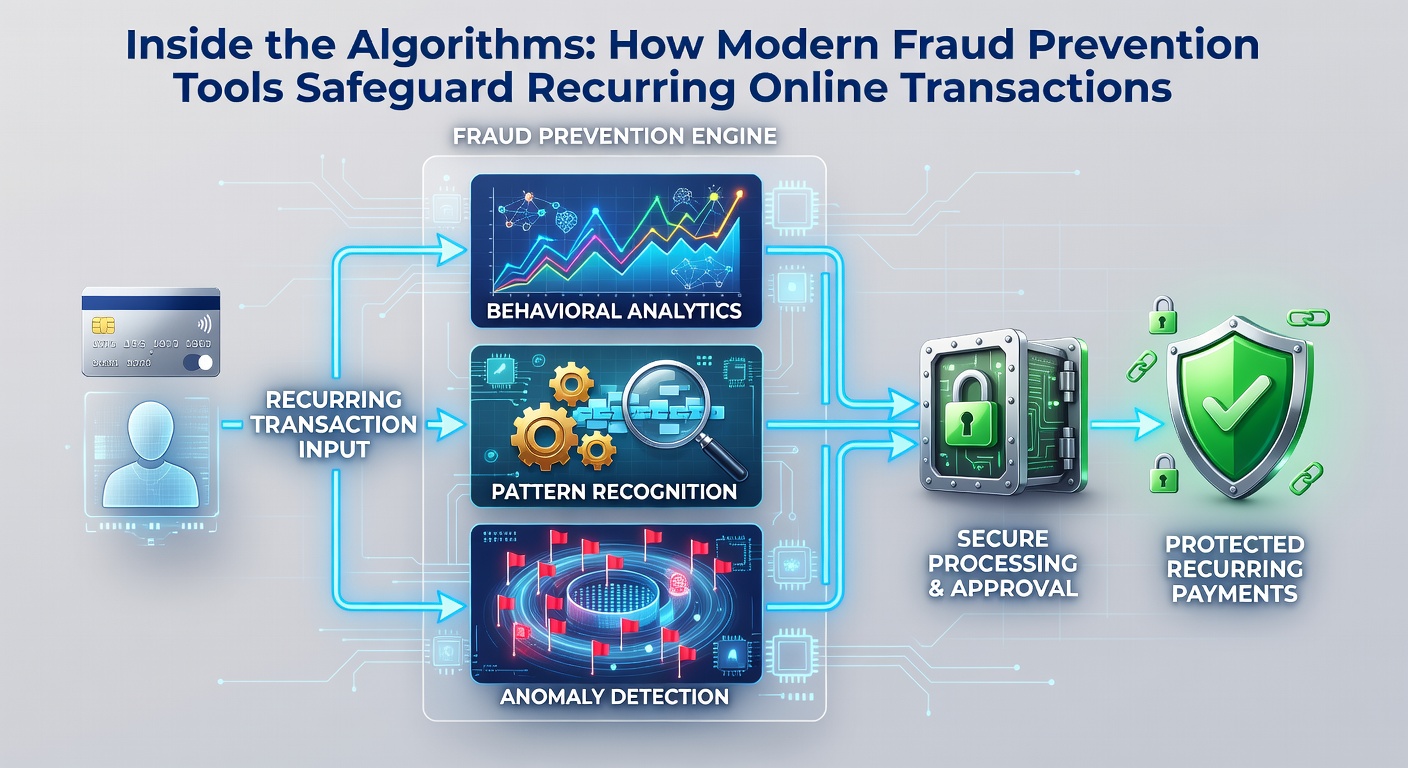

Modern fraud prevention tools rely on intricate algorithms that process vast datasets in real time, and these systems have become essential for merchants handling recurring online transactions such as subscriptions and automated billing cycles. Researchers have documented how machine learning models identify anomalies by comparing current transaction patterns against historical user behavior, while merchants deploy these tools to minimize chargebacks and maintain operational continuity.

Core Mechanisms in Algorithmic Fraud Detection

Algorithms begin by establishing baseline profiles for each customer through data points that include purchase frequency, device fingerprints, geographic locations, and payment method details. When a recurring charge occurs the system evaluates deviations such as unusual timing or mismatched IP addresses, then assigns risk scores that determine whether to approve, flag, or block the transaction. Observers note that these models continuously refine their parameters based on feedback loops from approved and declined activities, which allows them to adapt without manual intervention.

Behavioral analytics form another layer where velocity checks track the number of attempts within short windows and correlation engines link seemingly unrelated accounts that share similar characteristics. Data indicates that such layered approaches have reduced false positives significantly for merchants processing high volumes of subscription renewals, since the algorithms distinguish legitimate changes in billing cycles from coordinated fraud schemes.

Integration of Machine Learning and Real-Time Analytics

Merchants integrate supervised and unsupervised learning techniques so that labeled datasets train initial classifiers while clustering methods surface emerging threat vectors that lack prior examples. In May 2026 regulatory updates from the European Central Bank prompted many platforms to enhance their real-time analytics pipelines, and these changes aligned with new reporting requirements for cross-border recurring payments. The result has been tighter synchronization between fraud engines and payment gateways, which allows instant adjustments when transaction volumes spike unexpectedly.

Tokenization works alongside these models by replacing sensitive card details with unique identifiers that algorithms can validate without exposing full account numbers. When combined with device recognition and behavioral biometrics the overall framework becomes resilient against account takeover attempts that target recurring billing profiles. Those who have studied merchant implementations report that hybrid models incorporating both rule-based thresholds and neural network predictions deliver more consistent outcomes across different industry verticals.

Merchant Adoption Patterns and Industry Data

Smaller merchants often begin with off-the-shelf solutions that embed these algorithms into existing billing software, whereas larger operations build custom layers that feed internal data lakes directly into fraud scoring engines. Figures from the Reserve Bank of Australia reveal steady adoption rates among subscription-heavy sectors, particularly where monthly recurring revenue exceeds certain thresholds and exposure to international card networks increases. Merchants who link their analytics platforms to external threat intelligence feeds gain additional context about known compromised credentials or emerging botnet activity.

Case examples show that one subscription service provider reduced disputed transactions by integrating graph-based algorithms that map relationships between accounts and payment instruments. The approach identified clusters of synthetic identities that traditional velocity filters missed, and ongoing monitoring ensured that new accounts entering the system received appropriate scrutiny from day one.

Conclusion

Algorithms at the heart of contemporary fraud prevention tools continue to evolve through iterative training on fresh transaction data, and merchants benefit from the resulting improvements in accuracy and speed. Regulatory developments adn technological refinements work together to strengthen safeguards around recurring online transactions, while diverse data sources keep these systems responsive to shifting threat landscapes. Continued investment in these capabilities supports stable growth for businesses that depend on predictable billing cycles.